Unearned Revenue Journal Entry

Remember that income is not the assets ie. They need to record it as the unearned revenue which is the current liabilities.

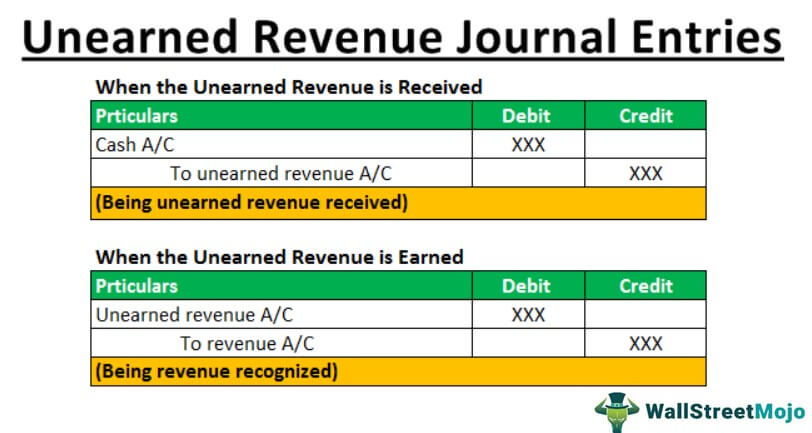

Unearned Revenue Journal Entry Double Entry Bookkeeping

A few examples of unearned revenue journal entries are stated below.

. Unbilled revenue is the amount that a company earns after goods or services deliver but not yet billed invoice to customers. The accounting equation Assets Liabilities Owners Equity means that the total assets of the business are always equal to the total liabilities plus the total equity of the business. The earned revenue is recognized with an adjusting journal entry called an accrual.

When cash receipts are received the cash account is debited or increased for the amount of the cash receipt. Its examples include an annual plan for the mobile. Journal Entry for Advance Received from Customer Example.

The seller records this payment as a liability because it has not yet been earned. Unearned revenue is money received by an individual or company for a service or product that has yet to be fulfilled. The amount received would be recorded as boos unearned income Unearned Income Unearned income refers to any additional earnings.

Journal Entry for Advance Received from a Customer. The following are examples of the deferred revenue Examples Of The Deferred Revenue Deferred revenue or unearned revenue is the number of advance payments that the company has received for the goods or services still pending for the delivery or provision. Deferred revenue is a payment from a customer for future goods or services.

Accounting Equation for Unearned Revenue Journal Entry. A corresponding credit is made to a revenue account such as for sales revenue a liability account unearned revenue an equity account common stock or another asset equipment. Likewise the company needs to properly make the journal entry for this type of advance payment as deferred revenue not revenue.

We can create chart of account customer deposit which is easy to control. At the end of the month the owner debits unearned revenue 400 and credits revenue 400. This is true at any time and applies to each transaction.

For deferred revenue the cash received is usually reported with an unearned revenue account which is a liability to record the goods or services owed to customers. The journal entry is debiting cash and credit unearned revenue. When there are more than two lines of entry in.

An adjusting journal entry is usually made at the end of an accounting period to recognize an income or expense in the period that it is incurred. Deferred Revenue Journal Entry Overview. The entity has concluded that the delivery of Product 1 and the performance of Service 1 are separate performance obligations and has allocated 500 of the contract revenue to Product 1 and 250 to Service 1 based on analysis and historical data.

Deferred revenue is common among software and insurance providers who require up-front payments in exchange for service periods that may last for many months. A properly documented journal entry consists of the correct date amounts to be debited and credited description of the transaction and a unique reference number. Examples of Deferred Revenue Journal Entry.

It is the revenue that the company has not earned yet. Recognition of Deferred. As a result journal entry for advance received from a.

On 1 st April a customer paid 5000 for installation services which will render in the next five months. The owner then decides to record the accrued revenue earned on a monthly basis. Unbilled Revenue Journal Entry.

These entries are typically made to record accrued income accrued expenses unearned revenue and prepaid expenses. Unearned revenue can be thought of as a prepayment for goods or services. In real life the company needs to perform service or deliver goods to the customers and process billing to collect money.

When the goods or services. The following journal entries are made to account for the contract. Remember in accounting we dont just list income as the account instead we list the exact type of income that took place which in this case is services rendered.

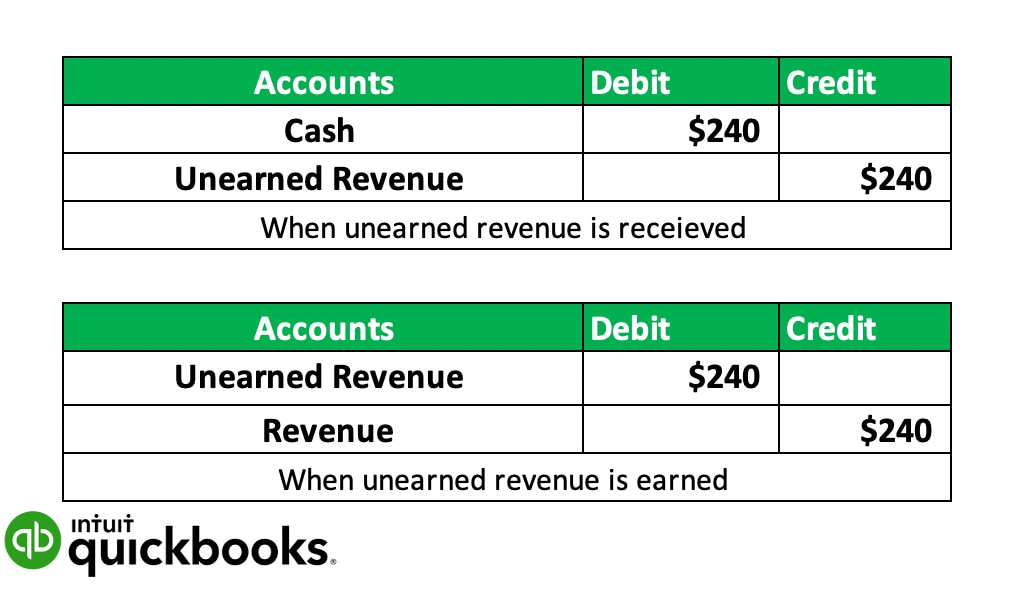

Deferred revenue is the payment the company received for the goods or services that it has yet to deliver or perform. The business owner enters 1200 as a debit to cash and 1200 as a credit to unearned revenue. Cash you get from for example rendering servicesIt is the event itself the rendering of the service that results in cash coming in immediately or at.

Unearned Revenue Journal Entry Examples. For this transaction the accounting equation is shown in the. In certain types of business transactions it is a requirement for the customer to pay a part of the total amount or the entire sum in advance for example security deposit to rent a property customized items bulk orders insurance premium etc.

ABC is a manufacturing that makes various types of clothes.

Unearned Revenue Journal Entries How To Record

Unearned Revenue Collect And Adjust Principlesofaccounting Com

What Is Unearned Revenue Quickbooks Canada

What Is Unearned Revenue Quickbooks Canada

No comments for "Unearned Revenue Journal Entry"

Post a Comment